3 Powerful Ways to Combat Home Affordability Challenges in 2023

webadmin • October 2, 2023

3 Powerful Ways to Combat Home Affordability Challenges in 2023

Are you worried that you can't afford even an entry-level home in your market today? You're not alone.

According to a recent survey by Divvy Homes, only 53% of Americans are confident in any way that they’ll be able to own their own home someday.

The study shows that the average American thinks it would take them between three and four years to afford a home - and a third believe it would take them five years or more. Another 20% expect that they’ll never be able to afford one.

Affordability is the overall problem: 63% of respondents said they often struggle to make ends meet, most commonly because of the high cost of living (69%) and rising inflation (56%).

Trust us, we want housing to become more affordable just as much as you do! Unfortunately, economic conditions are keeping homebuying costs higher for longer than we anticipated.

Today’s affordability challenges mean following the status quo when home shopping and making an offer just won’t cut it. You need to use every tool at your disposal to help make your new mortgage payment as affordable as possible!

This could mean finding creative ways to lower your monthly mortgage payment directly OR restructuring your overall debt picture, so a higher mortgage payment has less of an impact on your finances.

Our mortgage advisors have helped a lot of homebuyers strategize their mortgage financing to make a new mortgage payment more manageable in this market. Here are the top three strategies we believe are the most effective at improving home affordability in 2023.

Seller concessions are most commonly used to help reduce the buyer's out-of-pocket closing costs. However, when the goal is to make a mortgage payment more affordable in a high-rate environment, the best strategy is to use those concessions for a temporary rate buydown.

A temporary buydown gives you the option to lower your mortgage payment for one, two, or three years. The time period of the buydown depends on what your mortgage lender will allow and the amount of concessions you are able to get. The cost of the buydown depends on your loan amount and your interest rate (you can read this article to see how buydown costs are calculated).

After your loan closes, the funds for the buydown are placed in your escrow account (the same account that holds your prepaid taxes and insurance). Those funds are then used to reduce your mortgage payment every month until the buydown period is over.

For example, let's say you qualify for a mortgage at a 7.5% interest rate and are able to negotiate concessions to pay for a 2/1 buydown. For the first year of your mortgage, your monthly payment would be calculated at 5.5% interest instead of 7.5%. In the second year, your payment would be recalculated at 6.5% interest. After two years (the buydown period), your payment will return to 7.5% interest and stay there for the rest of the time you have that loan.

A temporary buydown is a great strategy to improve affordability in 2023 because mortgage rates are anticipated to come down. When that happens, you have the opportunity to refinance your mortgage to a permanently lower rate. And if you decide to refinance before the buydown period is over, you can use the remaining funds to reduce the cost of your refinance!

The amount of PMI you pay depends on the size of your down payment, your loan amount, your credit score, and your debt-to-income ratio. The fees typically range between 0.22% and 2.25% of your loan amount per year.

In addition to paying for a temporary buydown, seller concessions can also be used to completely remove or "buy out" the PMI on your loan. Depending on how much you are borrowing, this strategy could save you hundreds of dollars every month.

Just like a temporary buydown, your lender will tell you what the cost of the PMI buyout would be, and you would negotiate that amount in concessions from the seller. A PMI buyout could save you more than a temporary buydown, or vice versa.

Here's what the average American currently owes and pays monthly on credit cards, car loans, personal loans, and student loans:

Credit Cards

Personal Loans

Student Loans

Obviously, these numbers vary widely and depend on a variety of factors, but they do give us a good idea of just how much Americans are paying every month IN ADDITION to their housing payments. It's no wonder people feel like they can't afford a mortgage today!

This is why it's so critical for you and your mortgage advisor to look at your entire financial picture. Your down payment is not just a down payment - it is a tool that should be strategically used to help you purchase a home with the lowest total cost.

Often, this means using some of those funds to eliminate other high-interest debt. Let's take a look at an example:

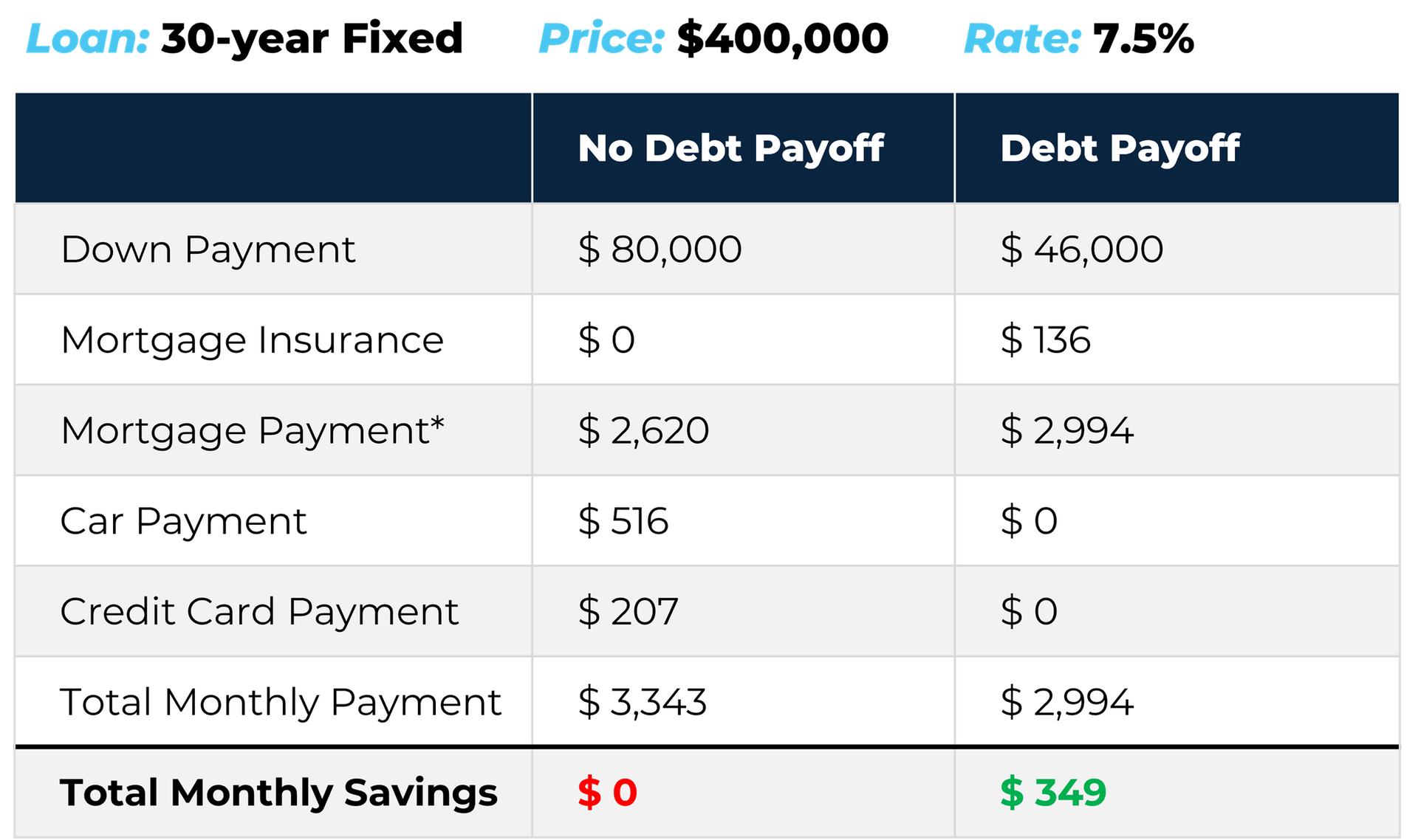

You want to buy a $400,000 home today with a 30-year fixed rate loan. With $80,000 down (20%) and a 7.5% interest rate, the estimated monthly payment on your new mortgage would be $2,620*.

You also have a car loan and credit card debt. The total balance on these debts is $33,699 with a total monthly payment of $723 (using the average amounts above). What would the impact be if you used some of your down payment to completely eliminate these other debts?

If you used $34,000 of your down payment to pay off your car loan and credit cards, you would have $46,000 left for an 11.5% down payment. This would increase your estimated monthly mortgage payment by $238 to $2,858*.

Putting less than 20% down would also force you to pay PMI. The estimated PMI percentage in this scenario is 0.46%, which would be $136 every month. This brings your total monthly mortgage payment to $2,994*.

So, putting less money down increased your mortgage payment by $374, but you were able to completely eliminate $723 in other monthly debt payments. You are now able to own a home and benefit from appreciation and a fixed housing payment while saving $349 a month!

Affordability is the overall problem: 63% of respondents said they often struggle to make ends meet, most commonly because of the high cost of living (69%) and rising inflation (56%).

Trust us, we want housing to become more affordable just as much as you do! Unfortunately, economic conditions are keeping homebuying costs higher for longer than we anticipated.

Today’s affordability challenges mean following the status quo when home shopping and making an offer just won’t cut it. You need to use every tool at your disposal to help make your new mortgage payment as affordable as possible!

This could mean finding creative ways to lower your monthly mortgage payment directly OR restructuring your overall debt picture, so a higher mortgage payment has less of an impact on your finances.

Our mortgage advisors have helped a lot of homebuyers strategize their mortgage financing to make a new mortgage payment more manageable in this market. Here are the top three strategies we believe are the most effective at improving home affordability in 2023.

1. Use seller concessions for a temporary rate buydown

When high mortgage rates dampen homebuying demand, it becomes more common for sellers to offer concessions to get their homes sold. According to Redfin, 42.9% of buyers received concessions from the seller in the first three months of 2023, which is close to the record high of 45.6%. These numbers are likely even higher now as higher rates have sidelined even more buyers.Seller concessions are most commonly used to help reduce the buyer's out-of-pocket closing costs. However, when the goal is to make a mortgage payment more affordable in a high-rate environment, the best strategy is to use those concessions for a temporary rate buydown.

A temporary buydown gives you the option to lower your mortgage payment for one, two, or three years. The time period of the buydown depends on what your mortgage lender will allow and the amount of concessions you are able to get. The cost of the buydown depends on your loan amount and your interest rate (you can read this article to see how buydown costs are calculated).

After your loan closes, the funds for the buydown are placed in your escrow account (the same account that holds your prepaid taxes and insurance). Those funds are then used to reduce your mortgage payment every month until the buydown period is over.

For example, let's say you qualify for a mortgage at a 7.5% interest rate and are able to negotiate concessions to pay for a 2/1 buydown. For the first year of your mortgage, your monthly payment would be calculated at 5.5% interest instead of 7.5%. In the second year, your payment would be recalculated at 6.5% interest. After two years (the buydown period), your payment will return to 7.5% interest and stay there for the rest of the time you have that loan.

A temporary buydown is a great strategy to improve affordability in 2023 because mortgage rates are anticipated to come down. When that happens, you have the opportunity to refinance your mortgage to a permanently lower rate. And if you decide to refinance before the buydown period is over, you can use the remaining funds to reduce the cost of your refinance!

2. Use seller concessions to eliminate private mortgage insurance

If you are buying a home with a conventional mortgage and do not have enough money saved for a 20% down payment, you will have to pay private mortgage insurance (PMI). This is insurance that protects the lender against losses if you are not able to repay your loan.The amount of PMI you pay depends on the size of your down payment, your loan amount, your credit score, and your debt-to-income ratio. The fees typically range between 0.22% and 2.25% of your loan amount per year.

In addition to paying for a temporary buydown, seller concessions can also be used to completely remove or "buy out" the PMI on your loan. Depending on how much you are borrowing, this strategy could save you hundreds of dollars every month.

Just like a temporary buydown, your lender will tell you what the cost of the PMI buyout would be, and you would negotiate that amount in concessions from the seller. A PMI buyout could save you more than a temporary buydown, or vice versa.

3. Reduce your down payment

This might seem counterintuitive - wouldn't less money down INCREASE your monthly mortgage payment? Aren't we trying to save money here? So many people are focused on getting their mortgage payment as low as possible that they forget to consider their overall financial picture. If your goal is to make a mortgage payment more affordable, you want to zoom out and take a look at your finances as a whole.Here's what the average American currently owes and pays monthly on credit cards, car loans, personal loans, and student loans:

Credit Cards

- Average credit card balance: $7,279 (lendingtree.com)

- Average credit card interest rate: 22.16% (lendingtree.com)

- Average credit card payment: $207 (interest + 1% of balance)

- Average used car loan balance: $26,420 (lendingtree.com)

- Average used car loan interest rate: 11.38% (nerdwallet.com)

- Average used car loan payment: $516 (lendingtree.com)

Personal Loans

- Average personal loan balance: $8,018 (lendingtree.com)

- Average personal loan interest rate: 18.35% (lendingtree.com)

- Average personal loan payment: $205 (3-year term)

Student Loans

- Average student loan balance: $37,338 (educationdata.org)

- Average student loan interest rate: 5.8% (educationdata.org)

- Average student loan payment: $503 (educationdata.org)

Obviously, these numbers vary widely and depend on a variety of factors, but they do give us a good idea of just how much Americans are paying every month IN ADDITION to their housing payments. It's no wonder people feel like they can't afford a mortgage today!

This is why it's so critical for you and your mortgage advisor to look at your entire financial picture. Your down payment is not just a down payment - it is a tool that should be strategically used to help you purchase a home with the lowest total cost.

Often, this means using some of those funds to eliminate other high-interest debt. Let's take a look at an example:

You want to buy a $400,000 home today with a 30-year fixed rate loan. With $80,000 down (20%) and a 7.5% interest rate, the estimated monthly payment on your new mortgage would be $2,620*.

You also have a car loan and credit card debt. The total balance on these debts is $33,699 with a total monthly payment of $723 (using the average amounts above). What would the impact be if you used some of your down payment to completely eliminate these other debts?

If you used $34,000 of your down payment to pay off your car loan and credit cards, you would have $46,000 left for an 11.5% down payment. This would increase your estimated monthly mortgage payment by $238 to $2,858*.

Putting less than 20% down would also force you to pay PMI. The estimated PMI percentage in this scenario is 0.46%, which would be $136 every month. This brings your total monthly mortgage payment to $2,994*.

So, putting less money down increased your mortgage payment by $374, but you were able to completely eliminate $723 in other monthly debt payments. You are now able to own a home and benefit from appreciation and a fixed housing payment while saving $349 a month!

The Bottom Line

Yes, buying a home in 2023 is more expensive than it has been in the past, but there are options available to combat affordability challenges and make your new mortgage payment less stressful on your wallet. By changing how you use seller concessions and your down payment, considering your overall debt picture, and focusing on total monthly payment rather than just rate, it's very possible you will be able to purchase a home in this market and start reaping the incredible benefits that homeownership brings.With a long-term plan for your home purchase that considers your overall financial picture – not just how low your mortgage rate can be – you can put your money to work for you, purchase your dream home, and set yourself up for financial success.

We understand that everyone’s situation is different. Before making any decisions on your homebuying plans, it’s crucial that you look at the numbers for your specific purchase scenario and financial situation. If you would like to see a loan comparison that clearly shows how much you could save on a mortgage payment with these different strategies, give us a call or fill out the form below to request a consultation with a mortgage advisor. *Estimated monthly mortgage payments reflect hypothetical Principal, Interest, Taxes and Insurance amounts rounded to the nearest dollar amount and do not include other possible fees. These figures are estimated based on a minimum credit score of 740. Figures and rates shown are for educational purposes only and do not reflect an official mortgage loan offer.

From first-time homebuyers looking to stop renting to seasoned investors expanding their portfolios, real estate offers powerful advantages over the stock market—especially in 2025. Let’s take a closer look at why now is the time to make your move.

At Luminate Bank, we believe knowledge is power, especially when it comes to your financial decisions. Let’s take a look at how tariffs are creating a “perfect storm” for the housing market — and what that means for you.

Luminate Bank is proud to welcome the NJ Lenders Team, a leading East Coast home lending organization, to the Luminate Bank community, integrating its home lending expertise into the Luminate Bank brand.